Let’s Bring Capital to Care

Lenders have a powerful opportunity to tap into a high-demand, undercapitalized market and strengthen the backbone of local economies by providing capital to child care owners and operators.

Many child care providers want to strengthen and grow their businesses and are credit-worthy borrowers, creating the potential for long-term financial relationships as their needs evolve.

The Capital Access Learning Lab, a partnership of Community Development Financial Institutions (CDFIs) and child care support organizations convened by LISC, conducted the Capital for Child Care Survey on the journeys and aspirations of over 400 child care business owners in 2025. Let’s dive into the data.

–– 01 ––

The Opportunity to Finance Care

The market demand for child care is outpacing supply nationwide.

Nearly 1 in 3 children that need child care don't have access to licensed care options

with demand (12.3M children needing care) far exceeding supply (8.7M licensed seats) across 43 states. This shortage creates substantial growth opportunities for providers ready to expand.

*Source: Child Care Aware of AmericaThere's a dynamic field of 98,807 home-based child care (aka family child care, or FCC) and 92,613 center-based care (CBC) owners working to meet market demand— over the past year, the number of these businesses grew by 1.6% and 4.8%, respectively.*

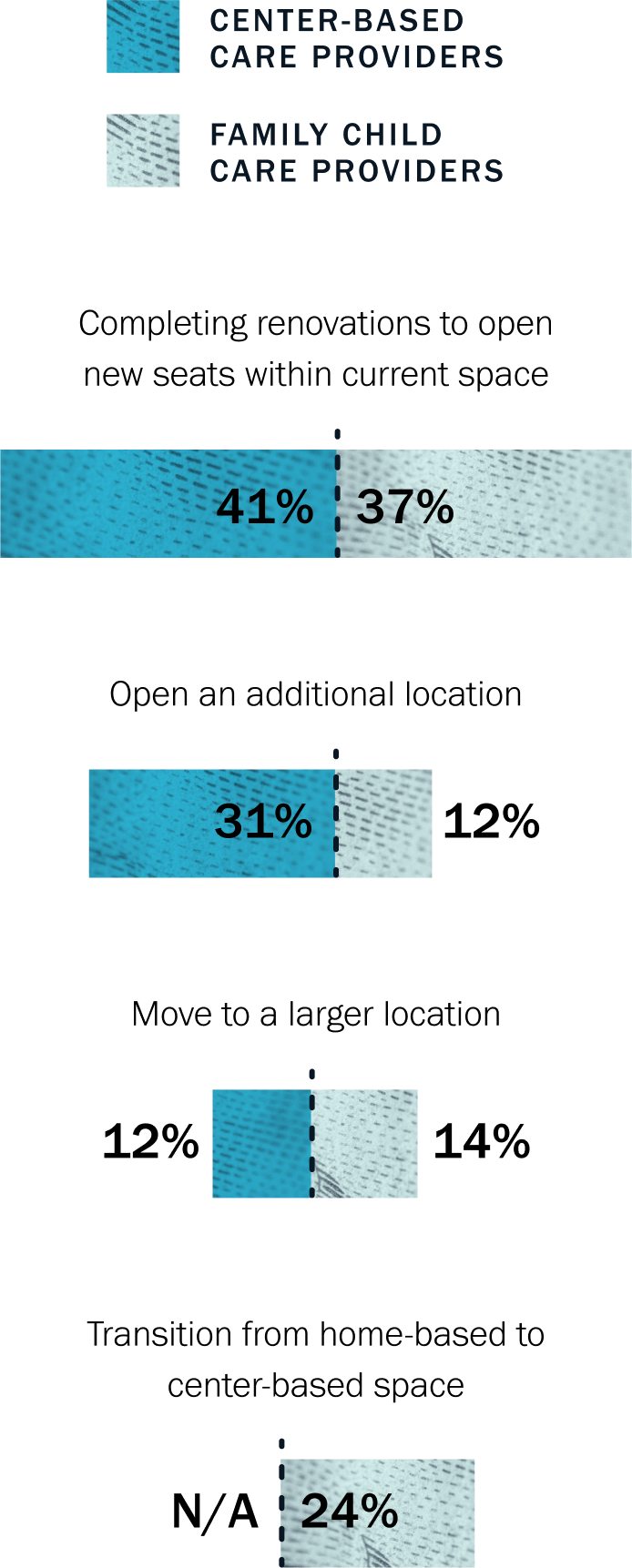

80% of surveyed business owners seek to grow in the next 5 years

How they plan to grow:

*Source: Capital for Child Care Survey

*Source: Capital for Child Care Survey

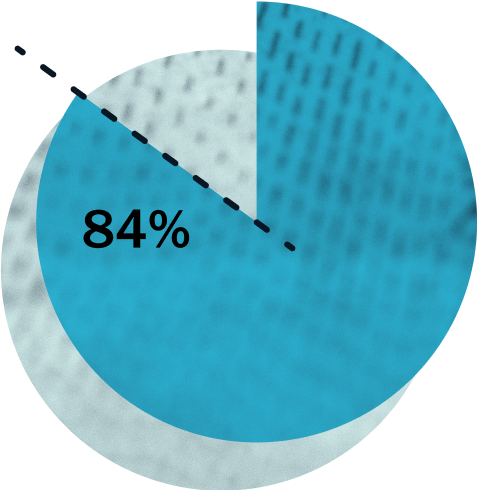

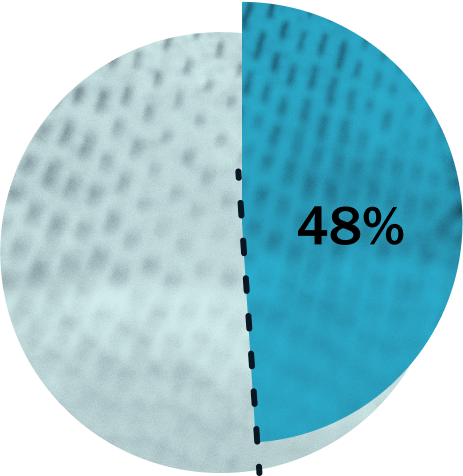

84% of all respondents say access to capital

would be the most helpful support in accomplishing their goals

Hiring/retaining staff, increasing number of children served, and expanding their space are the top goals that respondents said the capital would go towards

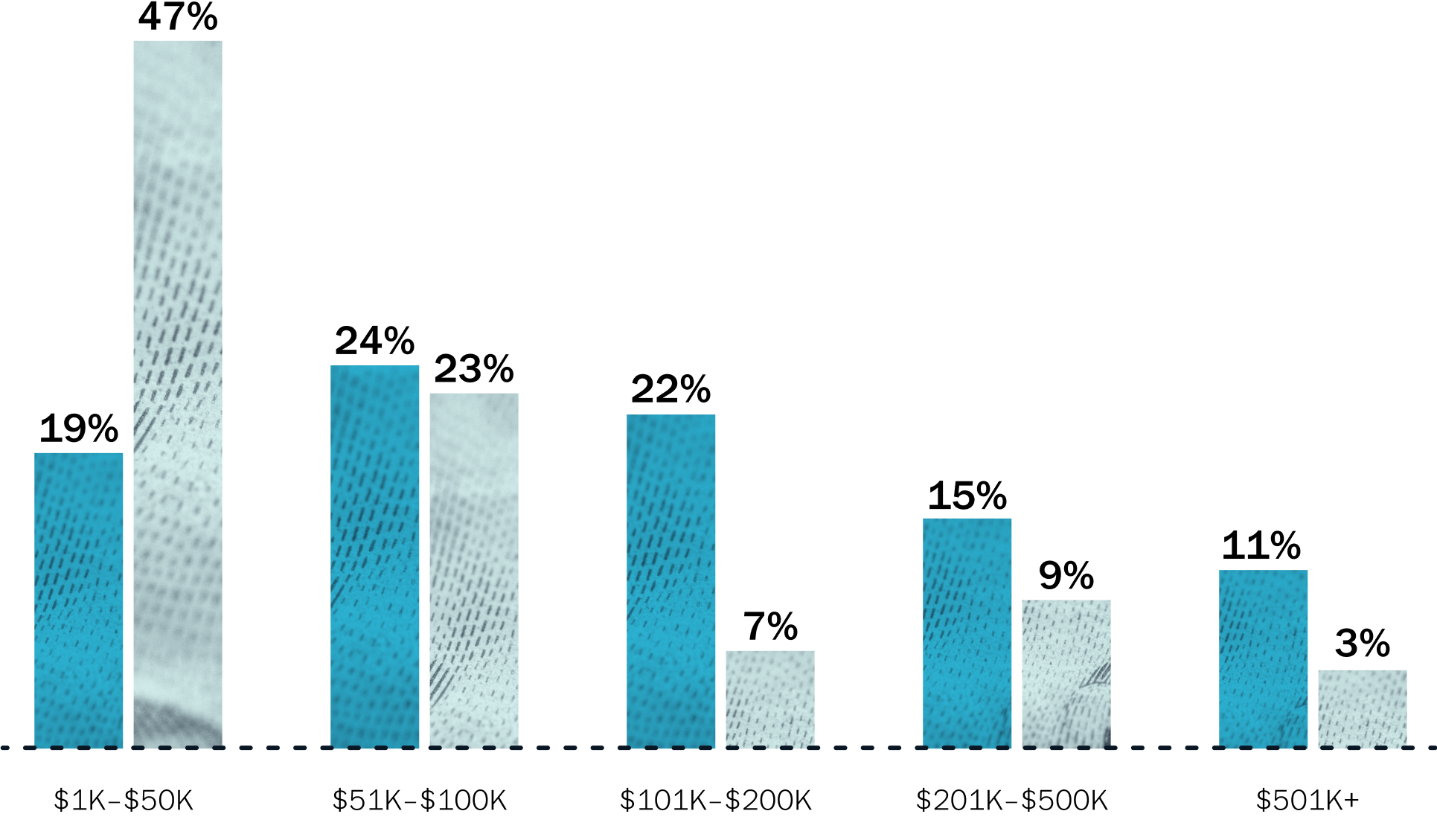

There is an estimated $37B in funding needed for child care providers to accomplish their goals. Here’s how much providers said they needed individually:

Scroll for more

Child care business owners are reliable, credit-worthy borrowers. They bring financial discipline and a deep sense of accountability to the families they serve.

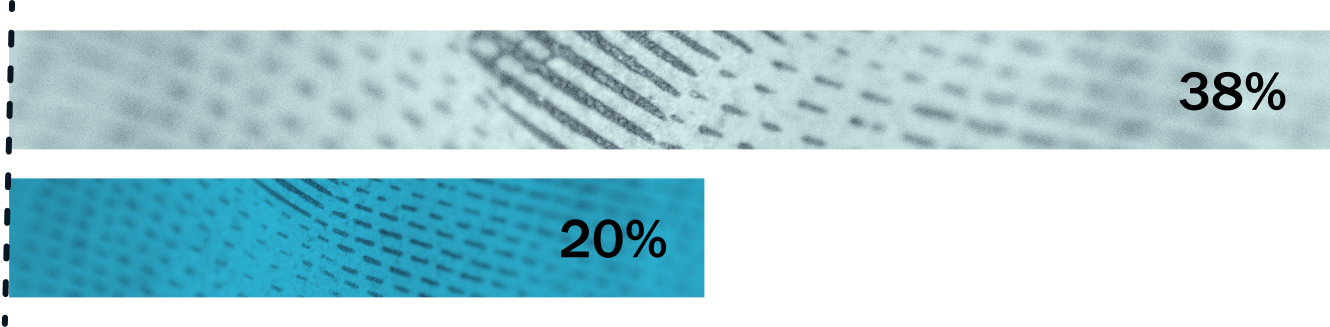

A national small business lender found that child care businesses were much more likely to repay their loans: only 20% went unpaid, compared to 38% of loans across all the other small businesses they served.

"I got a lot of no’s from banks when I tried to buy a building— I was deemed too risky as an FCC. But I did it anyway and now I run a profitable center."

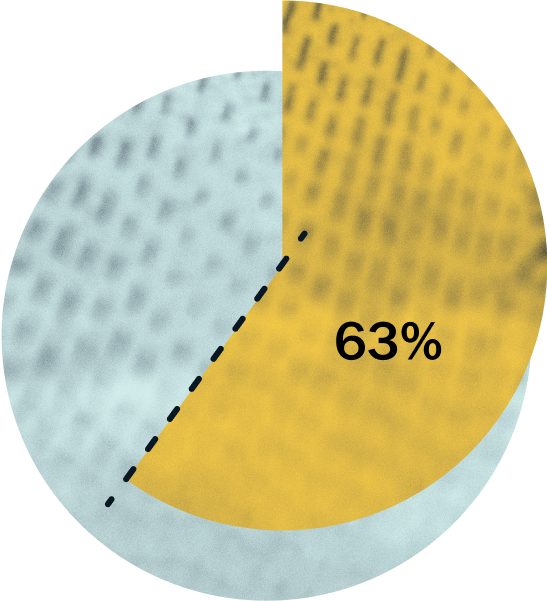

35% of CBC owners and 36% of FCC owners have predictable demand

with the majority of families they serve receiving federal, state, or local government subsidies or vouchers

*Source: Capital for Child Care SurveyWhen lenders finance child care, they support small businesses, strengthen local economies, and bolster care ecosystems.

59% of part-time or non-working parents say they would go back to work full-time if their child had access to quality child care at a reasonable cost.

*Source: First Five Years Fund

Adequate levels of child care would have netted the US economy $122 billion in gained earnings, productivity, and revenue in 2023.

*Source: ReadyNation, 2023

Quality birth-to-five education delivers a 13% annual return on investment, and shows lasting gains in IQ that drive better education, health, social, and economic outcomes.

*Source: Heckman Equation

Partnering with providers can help lenders fulfill Community Reinvestment Act (CRA) criteria, which supports low- and moderate-income communities meet their credit needs.

–– 02 ––

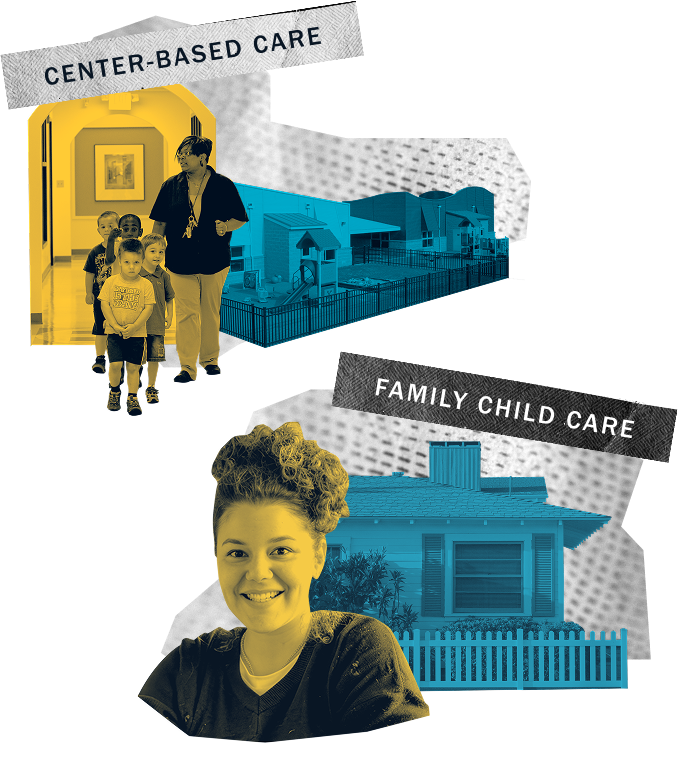

Child Care Business Owners

From solo home-based business owners to multi-site operators, there is a full spectrum of providers seeking capital.

33% of CBC and 32%* of FCC providers are currently growing their businesses**

(i.e. expanding capacity, improving quality, adding locations, adding state-funded pre-K, etc.)

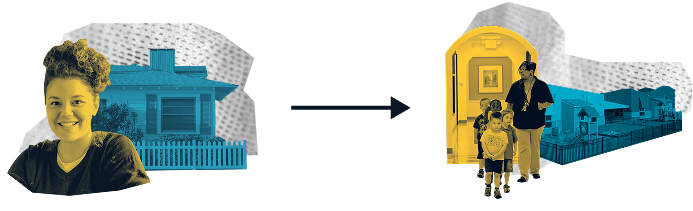

*This includes 7% of FCCs who are actively working to shift from home to center-based care

**This landscape centers on licenced care providers, and does not include the expansive network of unlicensed friends, family, and neighbors who provide high quality care to children across the country– another key component of the child care system.

Here are four provider profiles with clear demand, repayment potential, and room to grow.

FCC provider looking to expand in current home

Randi, who lives in a child care desert, consistently cares for four kids out of her home and takes drop ins. Her space is limited; in order to serve double the number of children, she has a desire to build out an infant room to accommodate for different aged children than her home is currently suited for.

Estimated capital need

$20K–$40K

FCC provider transitioning to operating a center

Latrice has run a small home-based child care for 15 years out of her mom’s house. The process of accreditation and support from a child care quality network program expanded her business aspiration to launch a center in addition to her home. When the right building becomes available, she wants to secure a loan to purchase and retrofit it.

Estimated capital need

$800K–$1M

Single-site CBC business owners looking to expand

Serena and Mike operate a for-profit center that serves 75 kids. They ran a home-based business for 20 years, but their participation in a community business cohort inspired them to take the leap to open a child care center in 2018. Right now, they would like to think about expanding, either to purchase a new center, or to add onto their existing space.

Estimated capital need

$150K–$300K

Multi-site CBC business owners looking to expand

Tia and her aunt run a for-profit child care business with three centers that serve 277 children. Tia has been savvy about securing 8 grants since she launched in 2021, and enrolled in a 12 week educator bootcamp from Child Care Aware. She wants to invest even more heavily in marketing and develop an outdoor space that can allow her to launch summer programs.

Estimated capital need

$200K–$250K

–– 03 ––

Types of Capital Support

There’s so much untapped opportunity for lending to child care providers. Right now, most business owners can only access limited, one-size-fits-all capital support options, if they have access at all.

Top capital supports child care business owners have used:

Forgivable Loans

(such as the federal Paycheck Protection Program (PPP) loans)

Working Capital/Line of Credit

(flexible financing for regular business or project-based expenses)

Commercial Mortgage

(a loan secured by commercial property, used to purchase, refinance, or renovate business real estate)

Microloans

(typically less than $50,000 to support small businesses, entrepreneurs, or new ventures)

Commercial

Real Estate

(for predevelopment expenses, acquisition costs, development, and construction fees)

Capital supports are not typically tailored to the unique realities of child care businesses, and many business owners face difficulties navigating these approaches to capital support.

“I got a $100,000 loan that had to be spent to the penny. I only needed $75K, but had to do the full $100K of spend. So I was taking an extra $25K of debt… Why? That was really frustrating, I had to add on more projects outside of what I planned.”

There's a big opportunity to serve business owners in ways that actually fit with their needs. Learn from those already leading the way.

Scroll for more

Access CDFI

$1K-250K small business term loans or bridge financing to cover working capital and facilities improvement for child care providers in Nevada. Access CDFI also provides technical assistance to its borrowers.

- working capital

- facility improvement

Accion Opportunity Fund (AOF)

Small business term loans of $5K-250K for working capital, debt refinancing, and leasehold improvements across US. AOF also provides free business advising, resources, and networks to small business owners.

- Working capital

- Facility improvement

CEI Maine

Low-interest loans up to $250K for child care business owners in Maine to support working capital and facilities improvement needs. CEI also provides technical assistance to its borrowers.

- Working capital

- Facility improvement

Children's Investment Fund

Predevelopment loans up to $350K, as well as capital grants between $200K-1M for facility repairs and renovations in Massachusetts. CIF also provides technical assistance to its grantees and borrowers.

- Working capital

- Facility improvement

- Predevelopment

First Children's Finance

$1K-50K loans for working capital, equipment acquisition, or repairs, as well as $50K-100K loans for expansion, gap capital, equipment acquisition, or repairs. FCF also provides technical assistance to its borrowers.

- Working capital

- Facility improvement

IFF

Flexible loans ranging from $10k to $6.5M, and comprehensive real estate support for providers across the Midwest. IFF's Learning Spaces program helps providers access capital for facilities improvements and offers dedicated technical assistance throughout the renovation process.

- Working capital

- Facility improvement

- Construction

- acquisition

LISC

Privately and federally funded pre-development and planning grants alongside flexible facilities loans ranging from $100K-$8M. LISC also provides technical assistance to its borrowers.

- Working capital

- Facility improvement

- predevelopment

- construction

- acquisition

Low Income Investment Fund (LIIF)

$500K-4M loans to help finance child care facility acquisition and construction nationwide; also provides grants of up to $2M to support acquisition, construction, renovation, pre-development, and start-up in California, Oregon, Texas, and New York.

- Working capital (Startup)

- Facility improvement

- Predevelopment

- construction

- acquisition

Reinvestment Fund

Planning, predevelopment, or facility improvement grants and up to $400K in capital grants, as well as access to working capital and bridge loans in Philadelphia. RF also provides technical assistance to its grantees and borrowers.

- Working capital

- Facility improvement

- predevelopment

Strong local lenders may also be providing essential capital to providers, and they bring contextual knowledge of applicable capital programs/incentives and deep community ties.

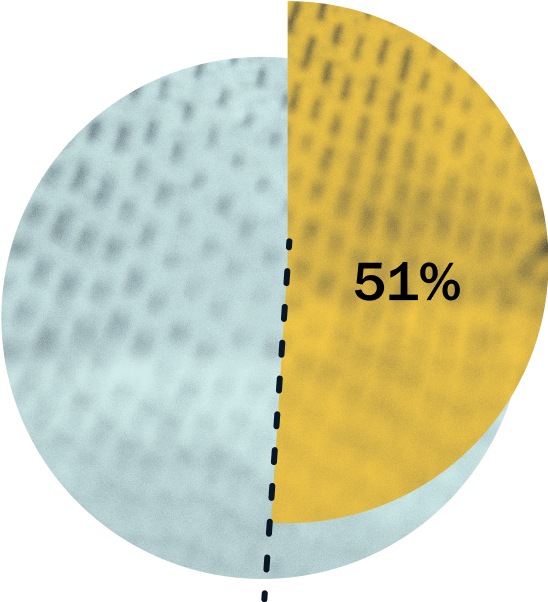

Supercharge capital with advisory expertise in running and operating child care businesses

Technical assistance (TA) in the form of business advisory is particularly valuable when it is informed by child care expertise. Lenders can dramatically improve financing outcomes by pairing their capital with this targeted TA from expert advisors.

51% of business owners say technical assistance would be helpful in achieving their current goals

*Source: Capital for Child Care Survey

"The loan came with a coach who understood my needs as a provider. When I told him what I wanted to do with the money, he was able to guide me in the process. I just wish the support would have continued for another year."

Highly desired TA subject areas for center-based business owners include:

- Improving quality (e.g., QRIS)

- Budgeting and planning for future income/expenses

- Planning educational activities/curriculum

- Managing day-to-day tasks (e.g., using tools or software to manage the business)

Here are examples of TA organizations lenders can partner with:

Scroll for more

Child Care Aware of America

Child Care Aware of America can help write local Child Care Resource & Referral (CCR&R) organizations into loan or grant agreements to deliver ongoing coaching at no cost to the lender

childcareaware.org

All Our Kin

All Our Kin operates a multi-week business coaching series for child care providers that lenders can plug in to shore up operators’ margins and bookkeeping so loan underwriting is cleaner and repayment risk is lower

allourkin.orgFirst Children’s Finance

First Children’s Finance can act as the formal TA arm in a credit package, preparing projections, monitoring covenants, and helping borrowers hit performance targets

firstchildrensfinance.orgLow Income Investment Fund

LIIF provides TA and training to help child care providers strengthen their financial capacity and readiness for loan underwriting and manages funds that provide grant capital to support leveraged financing for acquisition and construction projects

liifund.orgOpportunities Exchange

Opportunities Exchange can work with lenders as a thought partner to structure a business coaching initiative (e.g., establishing metrics, creating a budget, identifying a local partner)

oppex.orgLISC

LISC provides hands-on technical assistance (e.g., loan-readiness support), practical tools via the LISC Child Care Resource Library, and connections to local business partners and coaches

lisc.org.png)

National Association of Family Child Care

NAFCC offers strategies, including a new child care business accelerator & peer networking, to increase awareness of lending programs & improve child care provider readiness for loans

nafcc.orgLocal TA providers may also be excellent partners given expertise in local licensing, quality standards, and other requirements.

–– 04 ––

Take Action

Let's invest in the strength of our communities and get child care owners and operators the capital they need to thrive.

Lenders

Connect to a Referral Network

Are you a lender interested in financing child care businesses? Join our collaborative referral network to signal your interest and the types of deals you're looking for. Just complete our brief intake form and LISC, in partnership with a community of like‑minded lending partners, will keep an eye out for prospective borrowers who may align with your criteria.

Provider Referral Network FormChangemakers

Join a Community

Join the Capital Access Learning Lab, a growing coalition of CDFIs working to build the capital market child care business owners truly need. Through the Capital Access Learning Lab, you’ll co-develop new financial products, share data, and lead the way in shaping this emerging market. Fill out the intake form below to connect to this community.

Capital Access Learning Lab Intakeadvocates

Start

Advocating

The National Children’s Facilities Network (NCFN) is an advocacy coalition of financial institutions, technical assistance intermediaries and other stakeholders involved in financing high quality early care and education (ECE) facilities and businesses. Add your voice to NCFN and power a nationwide movement that opens funding doors for providers.

NCFN Membership Sign-up

About the Capital Access Learning Lab

Launched by LISC in 2025, the Capital Access Learning Lab brings together leading CDFIs and child care experts to dismantle the financial roadblocks that keep child care businesses from launching, scaling, and thriving. By combining deep lending expertise with on‑the‑ground sector knowledge, the cohort transforms real‑world insights into practical financing solutions that broaden capital access across the child care system.

Together, the Lab has interviewed providers nationwide, fielded a comprehensive survey, and co‑designed provider-facing products that honor the ingenuity and business savvy of child care entrepreneurs. The cohort convenes regularly to refine these ideas and champion policies and products that help every child care business secure the capital it needs to flourish.

Members of the Capital Access Learning Lab include:

Access CDFI, Accion Opportunity Fund, CEI Maine, First Children's Finance, IFF, LISC, Low Income Investment Fund, Reinvestment Fund, Child Care Aware of America, Home Grown, National Association of Family Child Care, Opportunities Exchange

Together, the Lab has interviewed providers nationwide, fielded a comprehensive survey, and co‑designed provider-facing products that honor the ingenuity and business savvy of child care entrepreneurs. The cohort convenes regularly to refine these ideas and champion policies and products that help every child care business secure the capital it needs to flourish.

Members of the Capital Access Learning Lab include:

Access CDFI, Accion Opportunity Fund, CEI Maine, First Children's Finance, IFF, LISC, Low Income Investment Fund, Reinvestment Fund, Child Care Aware of America, Home Grown, National Association of Family Child Care, Opportunities Exchange